Weekly Market Commentary

June 15th, 2026

Week in Review

The past week was highlighted by a landmark capital markets event, as SpaceX completed a record-setting initial public offering (IPO), alongside economic data that pointed to steady growth with persistent inflation pressures.

SpaceX completed the largest IPO in history, raising approximately $75 billion, far exceeding the prior record set by Saudi Aramco. Shares were priced at $135, opened at $150, and closed near $161, representing a first-day gain of roughly 19%. By the end of trading, the company’s market capitalization exceeded $2 trillion, compared to roughly $1.77 trillion at IPO pricing, immediately positioning it among the largest publicly traded companies globally.

Demand for the offering was substantial, with reports indicating the deal was multiple times oversubscribed and total investor interest exceeding $200 billion. The successful execution and strong initial trading reinforce that public markets remain highly receptive to large-scale issuers and could support additional IPO activity, particularly as other highly anticipated listings, such as Anthropic and OpenAI, are expected to come to market later this year.

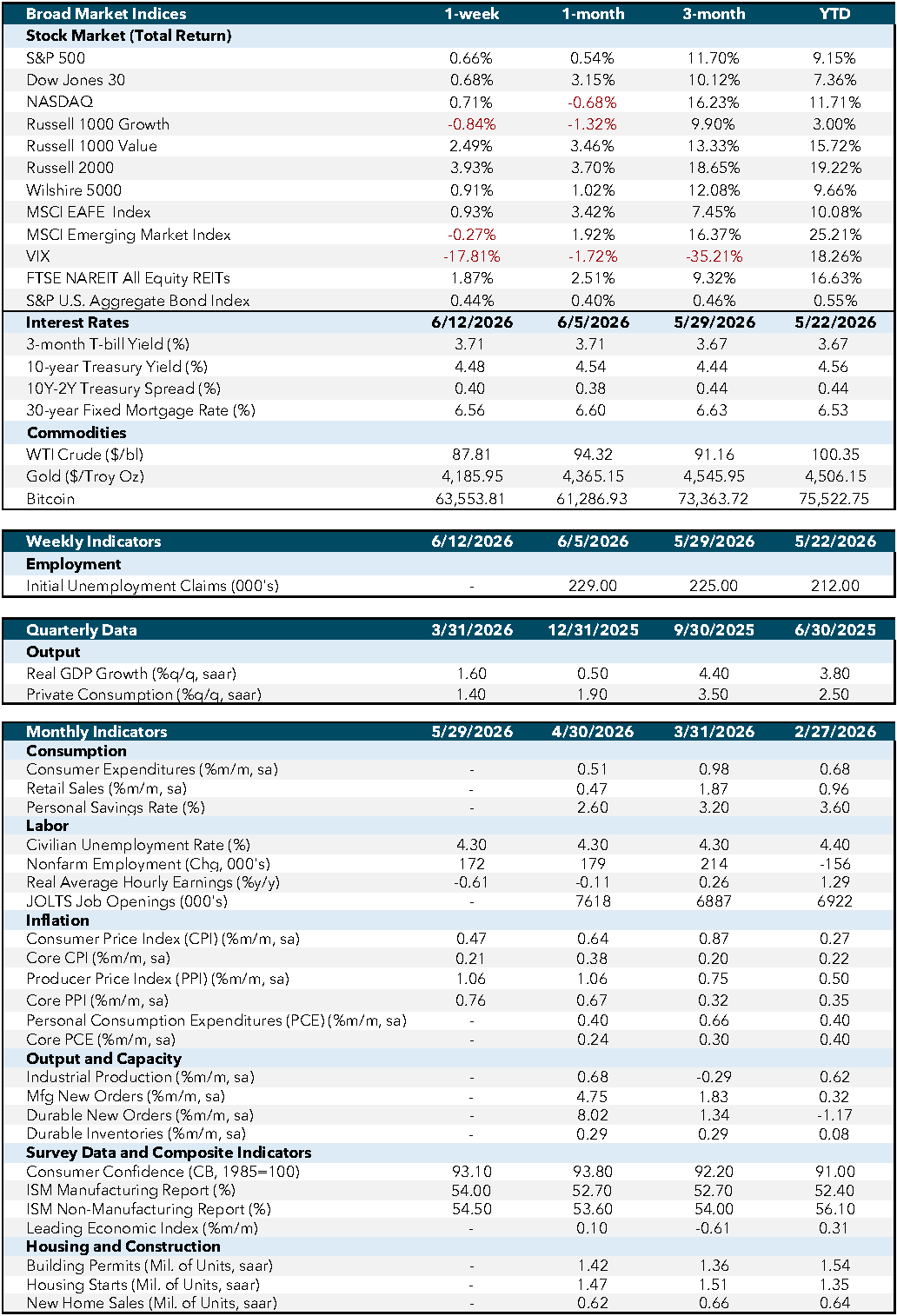

On the macro side, housing data came in stronger than expected, though the broader backdrop remains constrained. Existing home sales rose to 4.17 million, exceeding expectations near 4.07 million and marking a solid monthly increase. The upside surprise reflects continued resilience in demand, even as mortgage rates remain elevated.

Inflation data presented a more nuanced picture. The Consumer Price Index (CPI) increased 0.5% month-over-month and 4.2% year-over-year, in line with expectations and reaching a multi-year high. Much of the increase was driven by energy prices, which contributed significantly to the headline gain. In contrast, core CPI rose 0.2% month-over-month, below expectations, indicating that underlying inflation pressures remain more contained. This divergence suggests that recent inflation strength is being driven more by commodity-related factors rather than broad-based demand.

At the same time, producer price data indicates ongoing upstream pressure. The Producer Price Index (PPI) increased 1.1% month-over-month and 6.5% year-over-year, coming in above expectations and reflecting a sharp rise in goods prices, particularly energy-related components. This suggests that input costs remain firm, which could eventually pass through to consumer prices if sustained over the coming months.

Overall, last week’s developments reflect a market environment characterized by strong capital formation and steady economic activity, alongside persistent inflation dynamics. The success of the SpaceX IPO highlights continued strength in equity markets and investor demand, while economic data points to resilience in housing and an inflation backdrop that remains uneven.

Economic and Capital Markets Dashboard

Week Ahead…

The upcoming week will focus on consumer demand, energy markets, and monetary policy.

Retail sales will provide an updated read on consumer spending. In the prior release, sales rose modestly from the previous month following a stronger gain earlier in the quarter, indicating continued growth but some moderation in momentum. The next print will help clarify whether spending remains steady or is beginning to slow.

Crude oil inventories will offer insight into supply conditions. Recent data showed a notable draw in inventories, extending a multi-week decline and leaving stockpiles below typical seasonal levels. The upcoming release will indicate whether that trend of tightening supply continues or begins to stabilize.

The Federal Open Market Committee (FOMC) rate decision and projections will be the key event of the week. At the last meeting, the Fed held rates unchanged, citing solid economic activity alongside inflation that remains above target, with elevated uncertainty around the outlook. The updated projections will provide insight into how policymakers are assessing growth, inflation, and the expected path of rates following recent data.

Overall, the week’s releases should help refine the near-term outlook for consumption, inflation pressures, and policy direction.

Economic Indicators:

- CPI: Consumer Price Index measures the average change in prices paid by consumers for goods and services over time. Source: Bureau of Labor Statistics.

- Core CPI: Core Consumer Price Index excludes food and energy prices to provide a clearer picture of long-term inflation trends. Source: Bureau of Labor Statistics.

- PPI: Producer Price Index measures the average change in selling prices received by domestic producers for their output. Source: Bureau of Labor Statistics.

- Core PPI: Core Producer Price Index excludes food and energy prices to provide a clearer picture of long-term inflation trends. Source: Bureau of Labor Statistics.

- PCE: Personal Consumption Expenditures measure the average change in prices paid by consumers for goods and services. Source: Bureau of Economic Analysis.

- Core PCE: Core Personal Consumption Expenditures exclude food and energy prices to provide a clearer picture of long-term inflation trends. Source: Bureau of Economic Analysis.

- Industrial Production: Measures the output of the industrial sector, including manufacturing, mining, and utilities. Source: Federal Reserve.

- Mfg New Orders: Measures the value of new orders placed with manufacturers for durable and non-durable goods. Source: Census Bureau.

- Durable New Orders: Measures the value of new orders placed with manufacturers of durable goods. Source: Census Bureau.

- Durable Inventories: Measures the value of inventories held by manufacturers for durable goods. Source: Census Bureau.

- Consumer Confidence (CB, 1985=100): Measures the degree of optimism that consumers feel about the overall state of the economy and their personal financial situation. Source: Conference Board.

- ISM Manufacturing Report: Measures the economic health of the manufacturing sector based on surveys of purchasing managers. Source: Institute for Supply Management.

- ISM Non-Manufacturing Report: Measures the economic health of the non-manufacturing sector based on surveys of purchasing managers. Source: Institute for Supply Management.

- Leading Economic Index: Measures overall economic activity and predicts future economic trends. Source: Conference Board.

- Building Permits (Mil. of Units, saar): Measures the number of new residential building permits issued. Source: Census Bureau.

- Housing Starts (Mil. of Units, saar): Measures the number of new residential construction projects that have begun. Source: Census Bureau.

- New Home Sales (Mil. of Units, saar): Measures the number of newly constructed homes sold. Source: Census Bureau.

- SA: Seasonally adjusted.

- SAAR: Seasonally adjusted annual rate.

Market Indices & Indicators:

- S&P 500: A market-capitalization-weighted index of 500 leading publicly traded companies in the U.S., widely regarded as one of the best gauges of large U.S. stocks and the stock market overall.

- Dow Jones 30: Also known as the Dow Jones Industrial Average, it tracks the share price performance of 30 large, publicly traded U.S. companies, serving as a barometer of the stock market and economy.

- NASDAQ: The world’s first electronic stock exchange, primarily listing technology giants and operating 29 markets globally.

- Russell 1000 Growth: Measures the performance of large-cap growth segment of the U.S. equity universe, including companies with higher price-to-book ratios and growth metrics.

- Russell 1000 Value: Measures the performance of large-cap value segment of the U.S. equity universe, including companies with lower price-to-book ratios and growth metrics.

- Russell 2000: A market index composed of 2,000 small-cap companies, widely used as a benchmark for small-cap mutual funds.

- Wilshire 5000: A market-capitalization-weighted index capturing the performance of all American stocks actively traded in the U.S., representing the broadest measure of the U.S. stock market.

- MSCI EAFE Index: An equity index capturing large and mid-cap representation across developed markets countries around the world, excluding the U.S. and Canada.

- MSCI Emerging Market Index: Captures large and mid-cap representation across emerging markets countries, covering approximately 85% of the free float-adjusted market capitalization in each country.

- VIX: The CBOE Volatility Index measures the market’s expectations for volatility over the coming 30 days, often referred to as the “fear gauge.”

- FTSE NAREIT All Equity REITs: Measures the performance of all publicly traded equity real estate investment trusts (REITs) listed in the U.S., excluding mortgage REITs.

- S&P U.S. Aggregate Bond Index: Represents the performance of the U.S. investment-grade bond market, including government, corporate, mortgage-backed, and asset-backed securities.

- 3-Month T-bill Yield (%): The yield on U.S. Treasury bills with a maturity of three months, reflecting short-term interest rates.

- 10-Year Treasury Yield (%): The yield on U.S. Treasury bonds with a maturity of ten years, reflecting long-term interest rates.

- 10Y-2Y Treasury Spread (%): The difference between the yields on 10-year and 2-year U.S. Treasury bonds, often used as an indicator of economic expectations.

- WTI Crude ($/bl): The price per barrel of West Texas Intermediate crude oil, a benchmark for U.S. oil prices.

- Gold ($/Troy Oz): The price per troy ounce of gold, a standard measure for gold prices.

- Bitcoin: A decentralized digital currency without a central bank or single administrator, which can be sent from user to user on the peer-to-peer bitcoin network.

This content was developed by Cambridge from sources believed to be reliable. This content is provided for informational purposes only and should not be construed or acted upon as individualized investment advice. It should not be considered a recommendation or solicitation. Information is subject to change. Any forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice. The information in this material is not intended as tax or legal advice.

Investing involves risk. Depending on the different types of investments there may be varying degrees of risk. Socially responsible investing does not guarantee any amount of success. Clients and prospective clients should be prepared to bear investment loss including loss of original principal. Indices mentioned are unmanaged and cannot be invested into directly. Past performance is not a guarantee of future results.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange.

Securities offered through Cambridge Investment Research, Inc., a broker-dealer, member FINRA/SIPC, and investment advisory services offered through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Both are wholly-owned subsidiaries of Cambridge Investment Group, Inc. V.CIR.0626-2241